What is the most important thing you can do for building wealth?

Recently, Jeff Levine (@CPAPlanner) put this question out into the Twitterverse:

Question: Other than regularly saving and investing, what do you think is the single most important to achieving long-term financial success?

I'll go 1st… Establishing + maintaining good credit. It can save someone hundreds of thousands over the course of a lifetime.

— Jeff "The Buckinghammer" Levine, CPA/PFS, CFP® (@CPAPlanner) August 14, 2020

Too often when dealing with financial decisions, we try to overcomplicate what is best for us. We liked the simplicity of a single thing to focus on, so this week we are breaking down our version of the most important thing you can do in each decade to improve your financial journey.

Harness the power of compound interest while you’re young

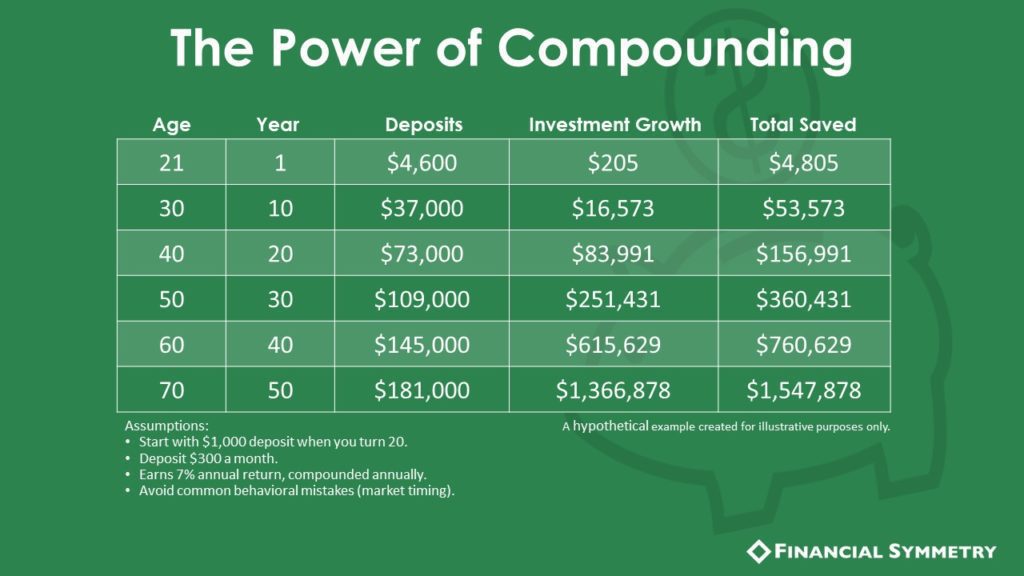

If you are starting to build wealth in your teens and 20s, you’re in luck. Time is on your side.

An often cited roadblock to getting this started, is the overwhelming debt obligations to student loans. While important to tackle high interest rate debt, carving out a small amount of automated savings can be life-changing.

For many, the first time we see a compound interest example, we are inspired. We included a powerful example below to demonstrate how much investment growth accumulates over 40 years, compared to the amount you are saving.

By saving small amounts early, compound interest becomes your super power. Automating this savings each month in an investment account with exposure to a diversified stock portfolio starting in your 20s, is arguably the single biggest impact decision you’ll make in building wealth. Because of the natural discipline it creates, making it harder to stop it down the road.

Continue to pay yourself first

During your 30s, life often becomes busier. Between new marriages, job changes and growing families, consequential decisions can pile up. These exciting changes bring curveballs you often don’t expect, like childcare for remote school over the past year.

This is when deciding to pay yourself first benefits you behind the scenes when the everyday life decisions are taking priority. If your saving and investing decisions are made only after you cover your expenses, then your budget is upside down.

Automating your savings and charitable giving can leave you better positioned as you head in to your 40s.

Don’t compare yourself with those around you

During this decade, it’s tempting to continue moving the goalposts as you reach certain levels of success.

Comparing your financial situation to others is a common derailment to your long-term success in your 40s. Keeping up with the Joneses can feel like an endless treadmill.

In the The Psychology of Money, Morgan Housel writes, “the ceiling of social comparison is so high that virtually no one will ever hit it, which means it is a battle that can never be won or that the only way to win is to not fight it to begin with, to accept that you might have enough even if it’s less than those around you.”

Determine your definition of enough. Is it a certain amount of money in the bank? A bigger house? Being laser focused on your ultimate financial goals, allows you stick to your financial plan, providing peace of mind along the way.

Be flexible in your 50s

Successful financial planning begins with understanding potential high impact risks.

More and more, we see unexpected hurdles for people in their 50s. It could be a layoff or a loss of assets due to grey divorce, but understanding the potential impact with scenario planning beforehand can leave you more agile to adjust.

Investing in your personal and professional relationships through the years, allows for more flexibility when reinventing yourself in these circumstances. Additionally, understanding the impact of withdrawals on your assets can be valuable in the case you need temporary withdrawals to sustain you during a transition.

After building wealth, keep perspective

Hopefully, in your 60s you are reflecting on a life well lived. This is a time to gain perspective. Common rules of thumb or family recommendations may not be the best. Some common things we hear related to this are:

- Because I’m retiring soon, shouldn’t I reduce the risk in my investment strategy?

- Don’t I need to pay off my mortgage before I retire?

- Shouldn’t I take Social Security at 62, because I not sure it will be there if I wait?

- Why would I want to make withdrawals from my IRA before I have to?

Having a plan in your 60s provides confidence, after income stops. When we have more time on our hands, worries can build tempting us to take unnecessary actions to protect our assets. Hiring a financial professional can help you develop a plan to gain perspective to best manage risks and seize opportunities on tax, investment, and estate planning for your assets.

To hear the most important moves in your 70s and 80s, check out the podcast episode at the top of this article.

Outline of This Episode

- [4:06] What is the one thing you can do in your teens and 20s to help build wealth?

- [8:23] The one thing in your 30s that you can do to build wealth

- [10:57] What should you be doing in your 40s to build wealth?

- [14:35] The one thing in your 50s that you can do to build wealth

- [17:49] What can you do in your 60s to build wealth?

- [21:30] Consider continuity in your 70s

- [22:55] What should you be doing in your 80s?

- [25:32] The progress principle

Resources & People Mentioned

- Jeff Levine on Twitter @CPAPlanner

- BOOK – The Psychology of Money by Morgan Housel

- BOOK – The Millionaire Next Door by Thomas J. Stanley

Connect With Chad and Mike

- https://www.financialsymmetry.com/podcast-archive/

- Connect on Twitter @csmithraleigh @TeamFSINC

- Follow Financial Symmetry on Facebook