There is a companion podcast for this post available. You can listen through the player above, or subscribe to our podcast on iTunes or Stitcher or Google Play.

There is a companion podcast for this post available. You can listen through the player above, or subscribe to our podcast on iTunes or Stitcher or Google Play.

Parents need to be wise about how they will pay for the increasingly high costs of college. That means many families should be applying for financial aid — and preparing their finances to get the most aid possible. With smart college planning, you can maximize your student’s financial aid eligibility.

Types of Aid

First, there are two main types of college aid: merit aid and need-based aid. Merit aid is straightforward — it is based on academic and extracurricular achievements. Students who excel in academics, sports or the arts can be awarded merit-based scholarships directly from their schools or through other institutions. Online tools such as Fastweb can help students seeking scholarship opportunities.

Need-based aid is more complicated. It depends on the student’s financial circumstances and can take the form of grant money, loans or work-study. Many affluent families assume that their children will be ineligible for need-based aid, but it often makes sense to apply anyway. By taking the right steps before the college-funding years, even affluent families may still qualify for a significant amount of aid. Plus, those who don’t qualify will still need to go through the federal student aid application process to receive federal loans.

Because finances are generally not considered for merit aid eligibility, the financial preparations you do will impact your student’s eligibility for need-based aid, whether it is federal or institutional.

Applying for need-based aid

To apply for federal need-based aid, families must complete theFree Application for Federal Student Aid, or FAFSA, which is administered by the government. To apply for institutional aid from almost 400 schools and programs, students must also complete the CSS Profile, administered by the College Board.

These forms collect information about your family’s finances to determine your expected family contribution, or EFC, the minimum amount your family is deemed able to contribute toward the cost of college. The amount of need that a student is eligible for is the cost of attendance less the EFC. The EFC takes into account factors like family size and the number of children in college, but the key drivers of aid eligibility are the income and assets of the parents and the student. Note that the FAFSA and CSS Profile use similar formulas, but the CSS Profile considers additional factors like home equity and small business ownership.

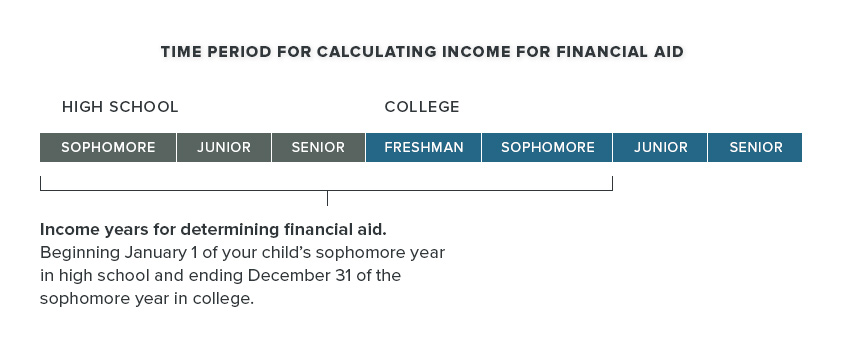

The FAFSA and CSS Profile are available in October of your child’s senior year of high school and each year thereafter until the year before they graduate from college. However, the income used to determine the level of need is based on the previous year’s tax return. For example, if your child starts college in the fall of 2017, your income will be based on your 2015 tax return. (These are recent changes for the FAFSA, which used to open in January and require the tax return information from the year immediately prior to enrolling.) The federal FAFSA deadline is in June, but deadlines vary for your state, school and the CSS Profile. Below is a chart showing the timing of your income and when it impacts financial aid eligibility.

How Income and Assets are Counted

For most families, the parents’ income will be the most important determinant for aid eligibility. Under the EFC formula for the FAFSA and CSS Profile, up to 47% of parents’ adjusted gross income is considered available for college funding. (Since this is progressive and there is an income allowance, it typically averages 20% to 25% of adjusted gross income for most families.) Up to 5.64% of nonretirement assets are counted, with a small allowance as well. Students are expected to contribute as much as 50% of their income and as much as 20% of their assets.

It’s important to note that your retirement assets are not counted in the calculation of EFC. Other assets like the value of small businesses, home equity and nonqualified annuities are not included on the FASFA either, but they are on the CSS Profile. However, in some cases, home equity is capped at 1.2 times the parent’s adjusted gross income on the CSS Profile.

Also note that parent and student assets are based on their market value at the time that you complete the aid forms. However, remember that you’ll be completing the financial aid forms annually, so as your financial situation changes so will your student’s aid eligibility.

Ways to Increase Aid Eligibility

There may be steps your family can take to increase your child’s chances of receiving the most student aid possible. Here are some strategies to consider:

- Max out your retirement accounts. While your child is younger, you can build up significant savings in retirement accounts, which will not be included in determining aid eligibility. In the year your student applies for aid, you’ll need to add contributions back into your income, but the assets still won’t be included for aid. Assets in a bank or brokerage account, on the other hand, would reduce aid eligibility.

- Pay down debt. Use taxable accounts like bank or brokerage accounts to pay down expensive credit card or student loan debt. This not only reduces your interest costs, but reduces your taxable assets, which can help increase aid eligibility. Since home equity is included for the CSS Profile, paying down your mortgage may not be the best strategy. But remember, FASFA does not consider home equity in determining aid and many CSS Profile schools place a cap on how much is counted.

- Reduce income. If possible, it helps to limit your income in years that are counted for financial aid. This is difficult to do if you have a regular salary, but you can watch out for selling assets that would trigger a large capital gain in your taxable accounts or look for ways to offset them with capital losses.

- Do not open custodial accounts for your children. Student assets are counted more heavily for financial aid purposes. If you already have custodial accounts, consider moving those assets to a 529 college savings plan for your child instead. Liquidating existing custodial accounts could result in capital gains, but you may still save more money in the long run. Since 529 assets are typically included at a lower rate than custodial accounts for financial aid, you’d want to run the numbers to see whether it is beneficial to make the move.

- Plan ahead for family contributions. Plan carefully if grandparents or other family members want to contribute toward college expenses. The amount and timing of this type of contribution can materially impact your child’s aid eligibility, so it’s critical to optimize such assistance.

Parents should also consider how aid is affected when they have more than one child in college. For instance, with two children in college, the parent’s expected family contribution is not twice what it would be for one child. In fact, the parents’ expected contribution is reduced for each child, though the percentage may differ on the FAFSA and CSS Profile.

Aid Packages

When a student qualifies for a certain amount of need-based aid, it doesn’t necessarily mean that the student will receive that much in the form of a grant. The college or university might not meet 100% of the student’s need or may offer a combination of grant money, work-study and/or loans. Schools also base some of their aid package decisions on how desirable the student is to the school, so it’s possible that the same financial information could produce very different aid packages from one school to the next.

You’ll find the information about the type and amount of aid the school is offering your student in financial aid award letters. It’s important to be sure you fully understand each type of aid being offered. You can compare award letters from different schools using the College Board’s online tool. If you are not happy with your aid results, you can always appeal, especially if your financial situation changes.

Also, keep in mind that to receive federal loans, you have to file the FASFA. Therefore, even if your income is too high for aid, but you would like your child to pay for a portion of college costs through federal loans, you should still complete this form.

Finding Your Strategy

College funding and admissions experiences are unique to each family. There are so many variables that even minor differences can have a dramatic impact on a family’s aid eligibility. Thus, it’s best to base your college planning and decisions on your situation only.

In some cases, the cost of a bad decision can be painful, especially when parents end up spending money on college at the expense of their own retirement. To develop a sound financial aid strategy, I recommend working with a fee-only financial planner who understands the process and the potential pitfalls. Applying for financial aid is complicated, and the wrong strategy can result in paying thousands of dollars extra for college.

A version of this article was published on NerdWallet.