For many people, evaluating their financial situation means just reviewing investment performance against the Dow Jones Industrial Average. Now, Morningstar has produced new research they call Gamma, which highlights the value of smart financial planning. This post will summarize the last of the five strategies, liability relative investing to prepare for inflation.

The research notes that “the purpose of the portfolio is to pay for an ongoing liability, which in the case of a retiree is to provide retirement income.” The “liability” of retirement income is obviously heavily influenced by inflation as one of the greatest risks in retirement is losing purchasing power over time.

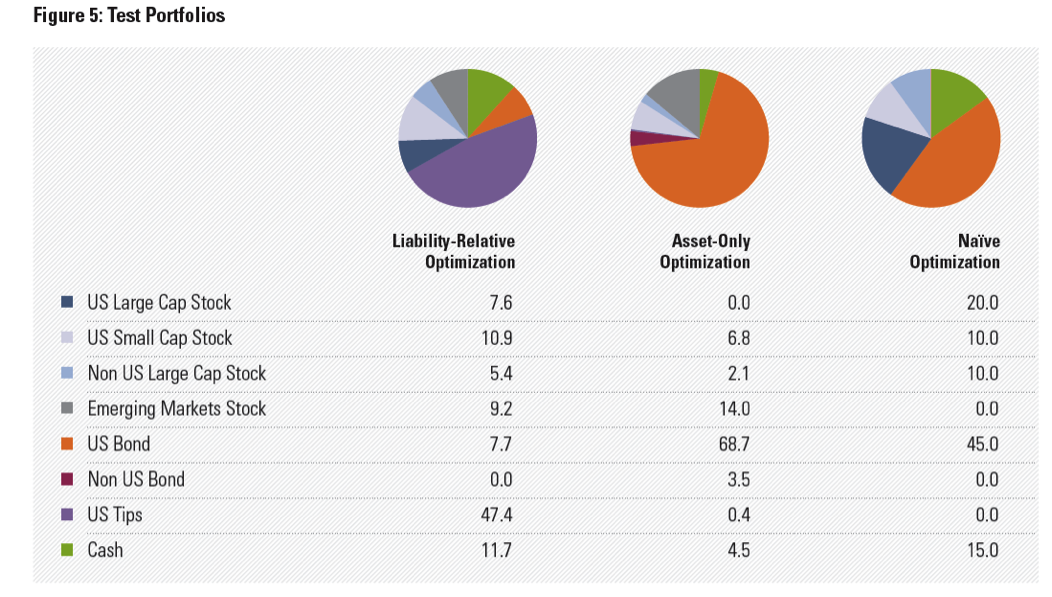

How Inflation Influences Your Portfolio

To illustrate this concept Morningstar compares the performance of 3 test portfolios under various inflation conditions. Their “Liability-Relative Portfolio” performs the best under medium to high inflation, most notably because of the high allocation to US TIPS at nearly 50%.

While this is a constructive point, you want your portfolio composition to be reflective of your overall cash flow needs; using the Liability Relative asset allocation they describe places a heavy bet on high inflation in retirement.

This seems a bit presumptive to put such a heavy allocation on inflation protected securities throughout retirement.

Instead, we would like to see this allocation adjusted throughout the retirement period based on market conditions and the economic environment, rather than a fixed assumption that inflation will be high.

Risk Capacity

This strategy relates closely back to asset allocation and using a risk level compatible with your goals. We feel that using a guide like our risk capacity model for portfolio construction and continuously monitoring those investments is more critical to long term success than making a particular bet on inflation conditions. The Morningstar analysis seems to reflect this as Liability Relative Optimization is the least impactful of the five factors, estimated to add only $.02 on every $1 of retirement income.

A Step in the Right Direction

Overall, the Gamma research is a step in the right direction toward measuring money managers by a metric other than investment performance. While producing alpha over long periods of time is achievable with a consistent strategy, it is impossible to deliver over every time period.

The benefit of making good financial planning decisions also extends far beyond the annual return on your investment portfolio.

This research identifies five factors that add to retirement income. However, we feel this is just the tip of the iceberg to what solid planning can achieve. In the context of retirement this is very powerful, but it also begs the question, how much value can be added if prudent strategies are applied throughout your career?