While most of our listeners are in or on the cusp of retirement, many are equally interested in helping their friends and loved ones in the next generation develop solid financial habits.

We often get questions about resources that could be helpful to inspire younger family members on their financial journey.

On this special International Women’s Day episode, you’ll meet our newest CFP®, Niamh Douglas. Niamh and Allison discuss some tools and strategies to help young people who are just starting out get off on the right financial foot.

3rd Decade

Unfortunately, sound personal finance habits are not consistently taught in schools or developed early in life.

Enter 3rd Decade, a two-year financial education program designed for young adults to establish a framework to help them develop a well-rounded understanding of key financial concepts.

3rd Decade Participants take four courses on personal finance topics like behavioral finance, assets and managing risk, taxes and retirement, and insurance.

Throughout the program, they also receive a few hours of financial mentoring from financial advisors who provide personalized counseling on:

- Establishing a consistent savings strategy

- Harnessing the power of compound interest

- Avoiding common behavioral mistakes

3rd Decade can help young people develop a thoughtful framework for making financial decisions that pays long term dividends.

Ways Young People Can Invest in Themselves

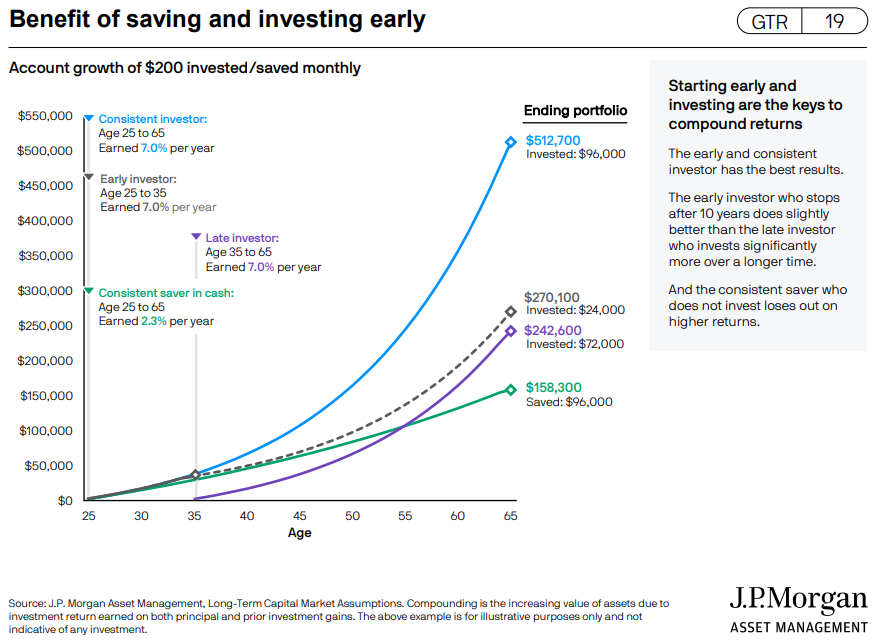

Recent graduates can find it challenging to develop a discipline around investing when retirement feels so far away. Luckily, very small investments early in your career can make an enormous impact long term. The following chart from JP Morgan illustrates this concept beautifully:

These benefits can be multiplied if you are a participant in an employer-sponsored plan that offers matching contributions. Sharing this information can make a powerful impact in the lives of your loved ones.

Listen in to hear more helpful resources that young people can use to build wealth and financial security.

Outline of This Episode

- [1:00] 9 Retirement surprises

- [2:11] Meet Niamh Douglas

- [4:14] About 3rd Decade

- [10:09] Ways young people can invest in themselves

- [16:11] Have financial family value conversations

- [18:03] Financial gift ideas for young women

Resources & People Mentioned

- Episode 189 – Smart Financial Decisions for Recent College Graduates

- 9 Retirement Surprises

- The Retirement Podcast Network

- 3rd Decade

- LadiesGetPaid.com

- Benefits of Saving & Investing Early [page 19] – JP Morgan Guide to Retirement

- BOOK – Simple Wealth, Inevitable Wealth by Nick Murray

- BOOK – Peaceful Prosperity by Laura Redfern